Alpha Research · Live Book

The diversified risk-premium book, paper-traded live

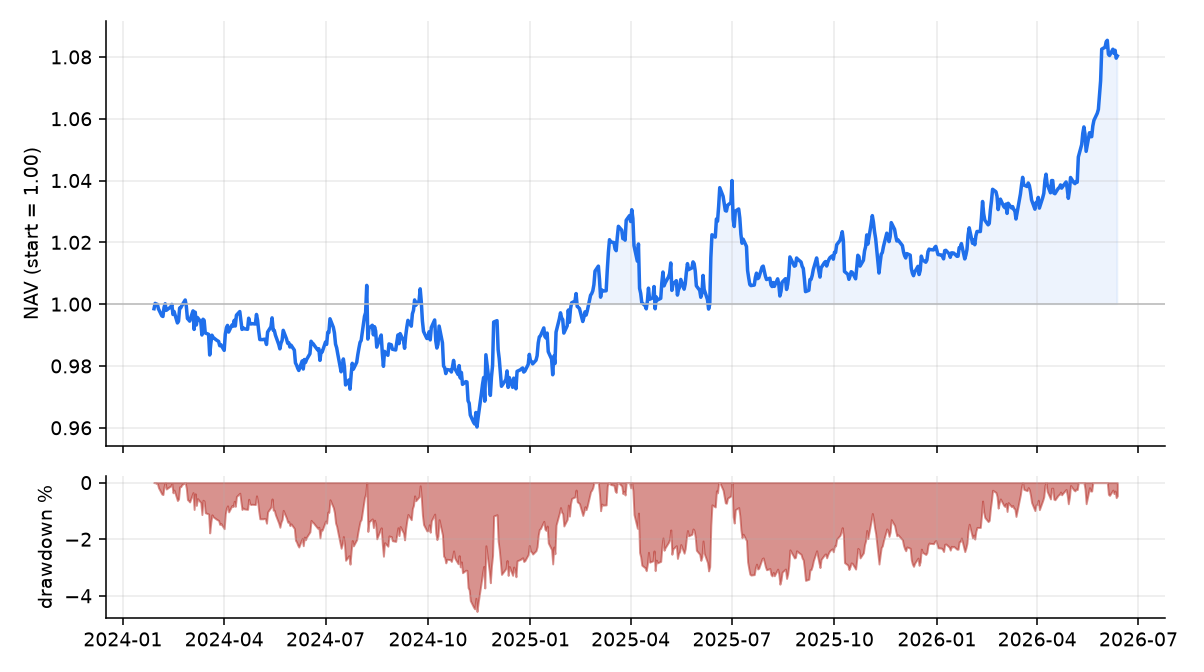

Inception 2024-01-01 · data through 2026-06-12 · updated 2026-06-17 17:11:42 UTC

The capstone of the Alpha Research series

(Paper 7), tracked forward as a paper portfolio.

NAV

1.080

Total return

+8.0%

Annualized

+3.2%

Sharpe

0.62

Volatility

5.3%

Max drawdown

-4.6%

Current target weights & sleeve performance

| Sleeve | Weight | Sharpe (since inception) |

|---|---|---|

| FX value | 48.5% | -0.59 |

| FX carry | 38.0% | +0.66 |

| Crypto funding carry | 8.8% | +1.12 |

| Crypto trend | 4.8% | +0.05 |

What this is. A risk-parity, 10%/yr-vol-targeted combination of the

daily-tradable survivors from the research program — crypto funding carry, crypto trend, and G10 FX

carry & value — each net of its own trading cost, recomputed daily and marked to current data. It is the

live, out-of-sample test of the program's thesis: that a handful of modest, near-uncorrelated risk premia

diversify into a respectable book. The premia are decaying, so this is the honest forward experiment, not a

backtest.

Caveats

- Paper-traded, not live capital — no broker, no real fills; capacity and borrow are largely internalized in the sleeve returns but not separately stress-modeled.

- Daily-tradable subset — equity quality & reversal are part of the full Paper-7 book but update monthly (Ken French) and need a broker/ETFs to trade daily, so they are tracked separately, not here.

- Realized volatility runs below the 10% target due to a leverage cap. Not investment advice.

The seven papers

1 Volatility Risk Premium · 2 Crypto Carry · 3 Crypto Stat-Arb · 4 The Cost of Direction · 5 Liquidity Provision · 6 FX & Commodity Carry · 7 Synthesis